Voluntary excess, Car insurance plays a crucial role in protecting you from financial burdens in case of accidents or damage to your vehicle. However, there’s a concept within car insurance policies that can sometimes be confusing: voluntary excess. This article dives deep into voluntary excess, explaining what it is, how it affects your premium, and the key considerations when choosing the right amount for your insurance needs.

What is Voluntary Excess?

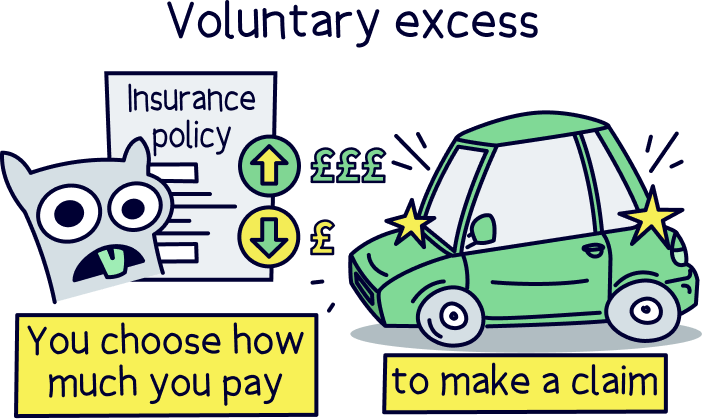

Voluntary excess, also known as voluntary deductible, is an amount you agree to pay out of pocket towards the cost of an insurance claim. It acts as a contribution you make alongside your insurer when your car suffers damage covered under your policy. There’s a crucial distinction between voluntary excess and compulsory excess (also known as compulsory deductible).

Compulsory Excess: This is a fixed amount mandated by your insurer that you must pay for any claim, regardless of whether you choose a voluntary excess. It’s designed to deter frivolous claims and manage insurance costs.

Voluntary Excess: This is an optional amount you can choose to add on top of the compulsory excess. By opting for a higher voluntary excess, you’re essentially agreeing to shoulder a larger portion of the claim cost. Here’s the catch: the reward for taking on this additional financial responsibility is a lower insurance premium.

How Does Voluntary Excess Affect Your Premium?

The relationship between voluntary excess and your insurance premium is straightforward: the higher the voluntary excess you choose, the lower your premium will be. This is because by agreeing to pay more out of pocket for claims, you reduce the insurer’s risk and potential payout.

Here’s an example to illustrate this concept:

Scenario 1: You choose a voluntary excess of ₹5,000. Your insurance premium might be ₹10,000.

Scenario 2: You choose a voluntary excess of ₹10,000. Your insurance premium might be ₹8,000 (due to a lower risk for the insurer).

In both scenarios, if you make a claim of ₹20,000:

Scenario 1: You would pay ₹5,000 (voluntary excess) + ₹10,000 (remaining claim amount paid by insurer) = ₹15,000 total.

Scenario 2: You would pay ₹10,000 (voluntary excess) + ₹10,000 (remaining claim amount paid by insurer) = ₹20,000 total.

While a lower premium is enticing, it’s crucial to choose a voluntary excess amount you’re comfortable paying in case of a claim.

Common Questions about Voluntary Excess on Google

A quick search on Google reveals some frequently asked questions regarding voluntary excess. Let’s address them here:

Is it always better to choose a higher voluntary excess?

Not necessarily. While a higher excess translates to a lower premium, consider your financial situation. If you can’t afford to pay a significant amount upfront in case of a claim, opting for a lower voluntary excess might be wiser.

What happens if the claim amount is less than the voluntary excess?

If the repair cost is lower than your chosen voluntary excess, you’ll shoulder the entire repair bill yourself. This is why it’s important to be realistic about the potential repair costs for your car’s value and typical driving conditions.

Can I change my voluntary excess after taking out the policy?

In some cases, insurers might allow you to modify your voluntary excess during the policy renewal period. However, this flexibility depends on your insurer’s policy and specific circumstances.

Does voluntary excess apply to all types of car insurance claims?

Voluntary excess typically applies to claims related to damage to your insured vehicle (own damage cover). For claims like theft or third-party damage, a separate excess amount might be applicable, so be sure to check your policy details.

Factors to Consider When Choosing Voluntary Excess

Here are some key factors to weigh when deciding on the right voluntary excess amount for your car insurance:

Your Budget: Evaluate your financial situation and how much you can comfortably afford to pay upfront in case of a claim.

Your Driving Habits: If you’re a cautious driver with a clean record, a higher voluntary excess might be a good option. Conversely, if you’re a new driver or someone prone to accidents, a lower excess might be more suitable.

The Value of Your Car: Consider the overall value of your car. For older vehicles with a lower market value, a higher excess might make sense. On the other hand, for expensive cars, a lower excess might be preferable to avoid a significant financial burden in case of damage.

FAQ’S

What is Voluntary Excess?

Voluntary excess, also known as voluntary deductible, is an amount you agree to pay out of your pocket towards an insurance claim. It’s like a pre-determined contribution you make before your insurer steps in to cover the rest. Think of it as your share of the financial burden.

Key Difference: Voluntary vs. Compulsory Excess

There’s another excess term floating around: compulsory excess. This is a fixed amount mandated by your insurer that you must pay for any claim. Voluntary excess, on the other hand, is optional. You choose to increase the excess amount on top of the compulsory one to enjoy a lower insurance premium.

Why Choose Voluntary Excess?

The primary reason to opt for a higher voluntary excess is to get a cheaper insurance premium. By agreeing to shoulder a bigger chunk of the claim cost, you become a less risky customer for the insurer, leading to a discount on your policy.

How Much Voluntary Excess Should I Choose?

This depends on several factors:

Your risk profile: Young drivers or those with a history of claims may be offered lower voluntary excess options.

Your car’s value: Expensive cars typically have higher excess amounts, both compulsory and voluntary.

Your budget: Can you comfortably afford the chosen voluntary excess in case of a claim?

Finding the Right Balance

While a higher voluntary excess translates to lower premiums, it’s crucial to choose an amount you can realistically pay if needed. Don’t get lured by a super low premium only to find yourself struggling to afford the excess during a claim.

Will a Voluntary Excess Affect My Coverage?

No, a voluntary excess doesn’t affect the type or extent of coverage provided by your insurance policy. It simply determines how much you contribute upfront before your insurer kicks in.

What Happens When I Make a Claim?

Let’s say you have a voluntary excess of ₹5,000 and your claim amount is ₹20,000. You’ll first pay ₹5,000, and your insurer will cover the remaining ₹15,000.

Is Voluntary Excess Applicable to All Insurance Types?

Voluntary excess is most commonly found in car insurance (often called voluntary deductible) but can also apply to other types like home insurance or travel insurance.

Things to Consider Before Choosing Voluntary Excess

Your driving habits: If you’re a frequent driver or prone to accidents, a high voluntary excess might not be the best idea.

The value of your insured item: For expensive cars or homes, a high excess could be a significant financial burden.

Your claims history: A clean claims history might allow you to choose a higher voluntary excess without worry.

Remember: It’s always wise to compare quotes with different voluntary excess options to find the one that best suits your budget and risk profile. Don’t hesitate to consult your insurance agent for personalized advice!

Bonus Tip: Some insurers offer tiered voluntary excess options. For example, you might have a lower excess for windscreen repairs and a higher one for major collisions. This allows you to customize your contribution based on the claim type.

To read more, Click here